Rationale

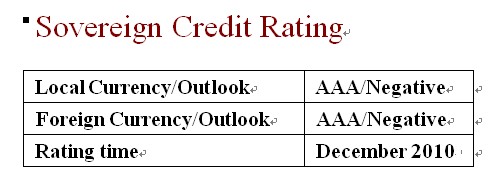

Dagong assigns “AAA” to both the local and foreign

currency long term sovereign credit ratings of the Republic of Finland (hereinafter referred to as

“Finland”) based on a comprehensive

analysis of such factors as its lower government debt burden and fiscal deficit,

relatively sound financial system but declining economic strength.

After experiencing the serious impact of the financial

crisis to the Finnish economy, the government fiscal deficit emerged and the

debt burden increased by 20%. However, compared with other European countries,

Finland’s debt burden and fiscal

deficit ratio are still quite low. By the end of 2009, the general government’s

outstanding debt reached 43.8% of GDP, far below the average level of 79.2% in

the Euro Zone and the EU’s warning line of 60%. Meanwhile, the government debt

structure is relatively reasonable, which is dominated by local currency and

long term debt, thus the debt repayment burden in the short term is weak. Under

the premise of current economic downturn, the government continues its

expansionary fiscal policy in 2010, and the extent of fiscal expansion will be

far more than that of other European countries. It is estimated that the fiscal

deficit will break through the EU warning line of 3% and reach 4.5% of GDP by

the end of 2010. The government’s financing requirement and debt-to-GDP ratio

will increase to 15.7% and 50% respectively. With the economic recovery and the

implementation of fiscal consolidation, the government’s fiscal deficit ratio

and debt ratio will hopefully be controlled within the EU criteria of 3% and 60%

respectively.

The Finnish economic development model based on

innovative exports has driven its economic prosperity for a decade with current

account surplus, fiscal surplus and sound financial system, etc. However, the

vulnerability in the exports structure and economic development has been fully

exposed under the financial crisis. Furthermore, the existing problems as high

welfare policy, aging trends and shortcomings in the financial system have

constrained the government’s fiscal and monetary adjustment capacity.

Nevertheless, the long-standing cumulative wealth and the government’s strong

financial capacity can still ensure the government’s debt repayment.

Specifically, it is summarized as follows:

l

That the

government actively promotes the independent innovative system is conducive to

the development of high-tech industries and to driving economic growth. However,

the consequent problems such as heavy dependency on global markets and excess

capacity also restrict the future economic potential to some extent.

l

The

economic development is in a high level, but the economy was severely affected

by the financial crisis due to the vulnerabilities in export destination and

product structure. Owing to the insufficient domestic and external demand, the

economic growth prospects in the next 3-5 years look quite gloomy.

l

The

financial system has less exposure to the toxic assets; it is steady and

adaptable to the economic development. The risks such as narrow profit margin,

liquidity and credit risks in the financial system are under control compared

with other European countries.

l

The

government’s high welfare policy and aging trend exacerbate the difficulties for

the fiscal situation to return to surplus. However, the government’s large

amount of net assets and the strong financing capacity in the European financial

market guarantee its capacity of debt repayment.

Outlook

Subject to the economic development model and exports

structure, the Finnish economy suffered significantly in the financial crisis.

Due to the insufficient domestic and external demand, the economic recovery and

growth prospects in the next several years look gloomy, which is unfavorable for

the increase of government revenues and ultimate improvement of the existing

fiscal deficit situation. At the same time, the high welfare and tax policy and

aging trend restrict the government’s capacity to adjust fiscal revenues and

expenditure, while the heavy dependency on wholesale funding and increasing

default ratio in household and commercial loans in the economic downturn will

increase the government’s contingent debt burden. Although the government net

assets are quite large and the financing capacity in the European financial

market is strong, yet these advantages are gradually eroded by the current

sovereign debt crisis happened in the EU and Finland’s slow

pace of economic recovery. As a result, Dagong keeps the negative outlook for

the Finnish government’s local and foreign currency credit rating in the next

1-2 years.

|